Skip to content

Skip to content

Key takeaways: 2027 Health Savings Account (HSA) contribution limits have been released, giving employers and employees updated figures to use in open enrollment planning. For 2027, individuals can contribute up to $4,500 and families up to $9,000, while catch-up contributions remain $1,000 for those age 55 and older. This announcement is critical to helping benefits teams prepare materials, systems, and compliance strategies for the year ahead.

- The 2027 HSA contribution limits increase to $4,500 for individual coverage and $9,000 for family coverage, with the $1,000 catch-up contribution unchanged.

- To remain HSA-qualified in 2027, HDHPs must meet updated deductible and out-of-pocket maximum requirements.

- Benefits teams should use these updates to refresh employee communications, payroll systems, and open enrollment planning materials.

Health Savings Accounts (HSAs) are a great way to help employees save for future healthcare costs and spend on qualified medical expenses. They are governed by Internal Revenue Service (IRS) rules, and while the regulations largely stay the same year after year, the IRS regularly updates the annual maximum contribution limits to keep pace with inflation.

What are the updated HSA contribution limits for 2027?

With the recent release of Revenue Procedure 2026-24,1 the IRS provided the 2027 inflation-adjusted HSA contribution limits. Plus, they gave an update on high-deductible health plans (HDHPs) and Excepted Benefit Health Reimbursement Arrangements (EBHRAs). Let’s walk through these updated figures so you can incorporate these adjustments into your benefits strategy for next year.

Here are the updated contribution limits for HSAs in 2027.

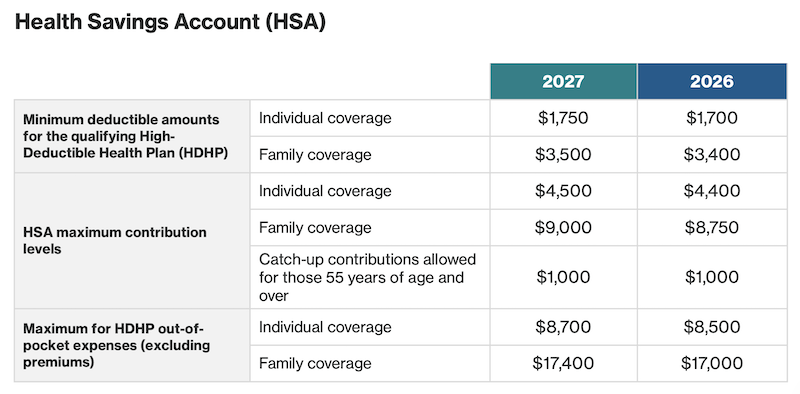

- Individual coverage: Individuals with high-deductible health plan (HDHP) coverage may now contribute a maximum of $4,500 to their HSA in 2027.

- Family coverage: For those with family HDHP coverage, the maximum HSA contribution limit increases to $9,000.

- Catch-up contributions: The HSA catch-up contribution limit remains $1,000 for eligible individuals age 55 or older.

What qualifies as an HDHP for 2027 HSA contributions?

To qualify as a high-deductible health plan under the 2027 rules, the plan must meet these criteria:

- Minimum deductible of $1,750 for individual coverage and $3,500 for family coverage.

- Maximum out-of-pocket expenses (excluding premiums) are capped at $8,700 for individual coverage and $17,400 for family coverage.

What is the inflation adjustment for EBHRAs in 2027?

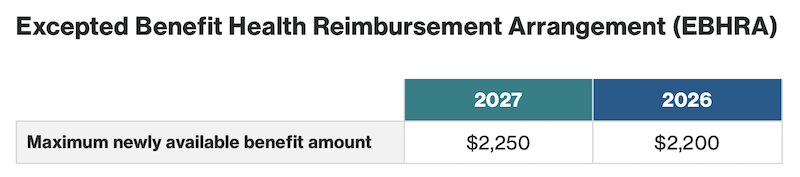

The maximum amount that may be newly made available for excepted benefit HRAs in 2027 has increased to $2,250, up from previous limit of $2,200.

What is the maximum fee for Direct Primary Care Service Arrangements (DPCSAs)?

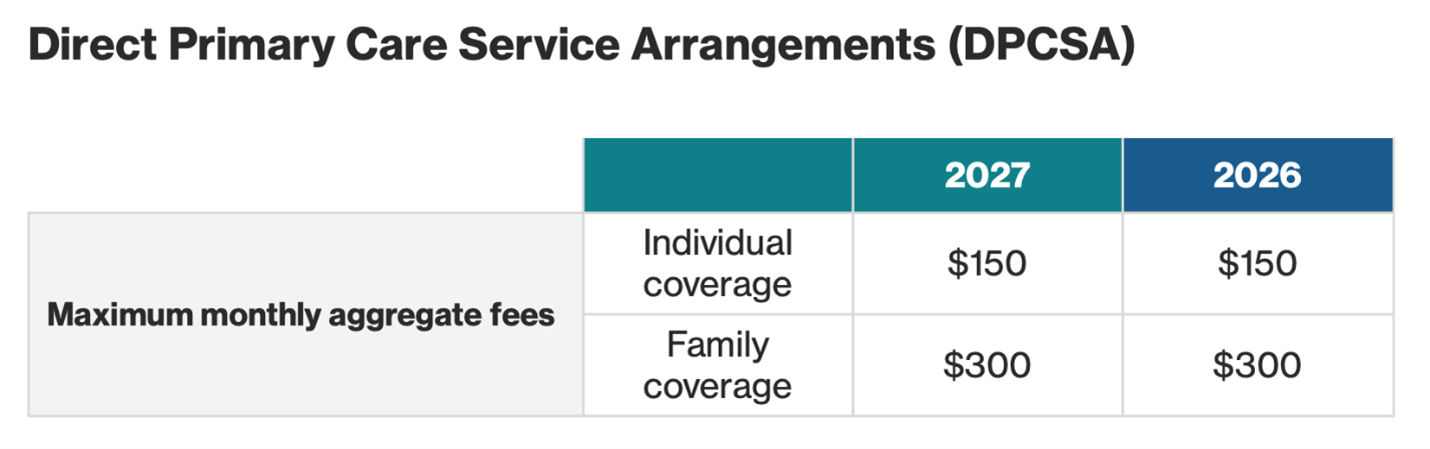

For 2027, the IRS has announced maximum monthly aggregate fees for all DPCSAs.2 The maximum is $150 for individuals and $300 for families, the same amounts that were allowed in 2026.

What other tax-advantaged accounts will have updated contribution limits for 2027?

While it has not yet been announced, the IRS usually publishes contribution limit updates for a number of other benefits accounts:

- Flexible Spending Accounts (FSAs)

- Dependent Care Flexible Spending Accounts (DCFSAs)

- Commuter benefit accounts

- Adoption assistance benefits

- Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

- Archer Medical Savings Account (MSA)

Limits on these types of accounts are typically announced in the fall of each year. You can find the current 2026 contribution limits here.

How do the updated HSA contribution limits help with open enrollment planning?

When the IRS updates its contribution limits, benefits teams also get to work updating their educational materials for employees. It’s critical that this information be shared with employees as they plan for open enrollment and adjust their personal contributions.

Here are three ways you can integrate the 2027 contribution limit updates into your benefits strategy:

1. Communicate the changes: Update your benefits guide and materials, and distribute them in multiple channels targeted to different employee groups. For example, Gen Z employees might be more likely to engage with on-demand videos, while those nearing retirement will want to hear about catch-up contribution limits. HealthEquity’s Open Enrollment Toolkit for employers is a great place to start.

2. Update payroll and benefits administration systems and work with your software partners to align your systems with the new contribution limits. This will help you ensure both individual and family contributions are accurately tracked and taxed appropriately.

3. Stay ahead of compliance by making sure your company’s HDHPs meet the required minimum deductible and out-of-pocket maximums for 2027. Subscribe to Remark Blog to keep informed of regulatory changes in the benefits industry.

Benefits teams are busier than ever as they approach Open Enrollment. Incorporating these regulatory updates into your planning process can help you stay ahead of the changes. Subscribe to the Remark blog for more insights into HR, benefits, and regulations that affect you and your people.

FAQs

What is the HSA contribution limit for individual coverage in 2027?

For 2027, the IRS has raised the maximum HSA contribution for individuals with high-deductible health plan (HDHP) coverage to $4,500. This is an inflation-adjusted increase designed to help individuals set aside more tax-advantaged dollars for healthcare costs.

What is the HSA contribution limit for family coverage in 2027?

For 2027, the IRS has set the maximum HSA contribution limit for family HDHP coverage at $9,000. This is an inflation-adjusted increase designed to help families set aside more tax-advantaged dollars for healthcare costs.

What is the HSA catch-up contribution limit for 2027?

For 2027, the HSA catch-up contribution limits are unchanged. An additional $1,000 can be contributed for individuals aged 55 and older, whether they have individual or family coverage.

HealthEquity does not provide legal, tax, or financial advice.

Subscribe to Remark Blog

Get new posts delivered to your inbox.

*Indicates a required field

Thank you for subscribing!